Homeowner’s insurance is a vital safeguard for major losses, covering catastrophic events rather

than everyday wear and tear. Understanding this distinction can help prevent misunderstandings and ensure your policy serves its intended purpose.

What’s Covered vs. What’s Not

Homeowner’s insurance protects against sudden, accidental events like fires, storms, or theft, but it doesn’t cover maintenance issues like aging roofs, deteriorating plumbing, or worn-out

systems. These are considered “wear and tear” and are the homeowner’s responsibility. Think of

it like health insurance: just as it doesn’t cover everyday actions like eating well or exercising,

homeowner’s insurance doesn’t cover routine upkeep. Both types of insurance focus on major,

unexpected events, not ongoing maintenance.

For example, if a roof develops leaks due to age, this won’t be covered. But if a storm

damages the roof, which could be eligible for a claim.

Tips for Roof Maintenance

While insurance doesn’t cover roof maintenance, proactive care can help prevent costly repairs.

Here are some quick tips:

- Inspect regularly for damaged shingles, especially after storms.

- Clean gutters to prevent water buildup.

- Trim branches near the roof to avoid scraping.

- Clear debris like moss and leaves, which trap moisture.

- Ensure proper attic ventilation to reduce mold risk.

Taking these steps can extend your roof’s life and reduce the chance of unexpected issues.

Older Roofs and Insurance Limitations

Many insurers are cautious about covering homes with roofs older than 10 years. Some may

decline new coverage for these homes or switch the policy terms from Replacement Cost (RCV)

to Actual Cash Value (ACV), paying only the depreciated value rather than full replacement. If

your roof is nearing the 10-year mark, consider an inspection or replacement to maintain

favorable coverage.

Unsure how your roof’s age might affect your policy? Reach out to discuss your options.

Actual Cash Value (ACV) vs. Replacement Cost (RCV)

ACV coverage considers depreciation and pays the roof’s current value, while RCV covers the

full cost of replacing it. RCV is often recommended for better protection against major losses.

Not sure which coverage is right for your home? Contact us to discuss whether ACV or RCV

aligns with your needs.

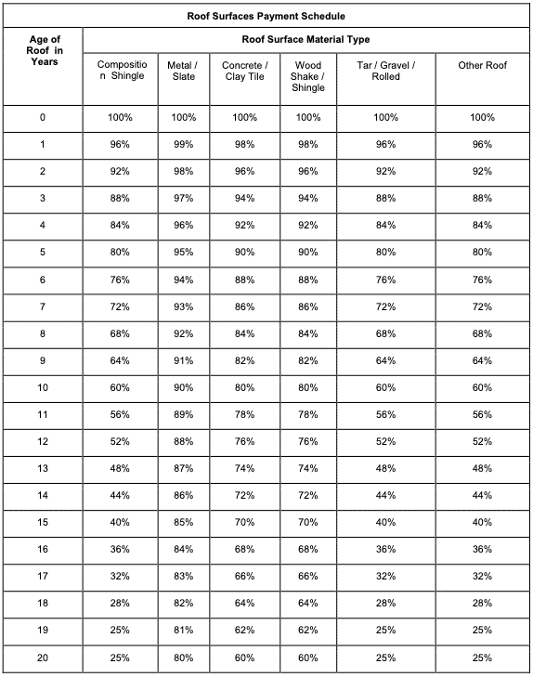

How Do Roof Payment Schedules Work?

The Roof Surfaces Payment Schedule shows how ACV roof coverage decreases as the roof ages.

For example, a 10-year-old composite shingle roof may be covered at only 52% of its

replacement cost. This schedule reflects how ACV considers age and wear, impacting payout

amounts.

Why Insurance Focuses on Catastrophic Losses

Insurance is a safety net for significant, unexpected events. While it doesn’t cover regular

maintenance, choosing RCV coverage can help protect you from major financial losses in a

catastrophe. Remember: insurance is about preparing for the unexpected, not replacing routine

upkeep.